Is Getting A Cfp Certification Worth It For Financial Advisors

Is Getting a CFP Certification Worth It For Financial Advisors?

Let’s cut to the chase. You’re a financial advisor, or maybe you’re thinking about becoming one. And you’re staring down this CFP certification. Is it just another piece of paper to hang on the wall, or is it the golden ticket? Honestly, the answer isn’t a simple yes or no. It’s a “well, it depends,” but let’s dig deep and figure out what it depends on for you.

I’ve seen advisors chase this thing like it’s the only way to succeed, and others who scoff at the idea. So, what’s the real deal? Is this prestigious certification worth the blood, sweat, and tears? We’re going to break down the good, the bad, and the ugly, so you can make an informed call.

The Hard Truth About the CFP® Mark

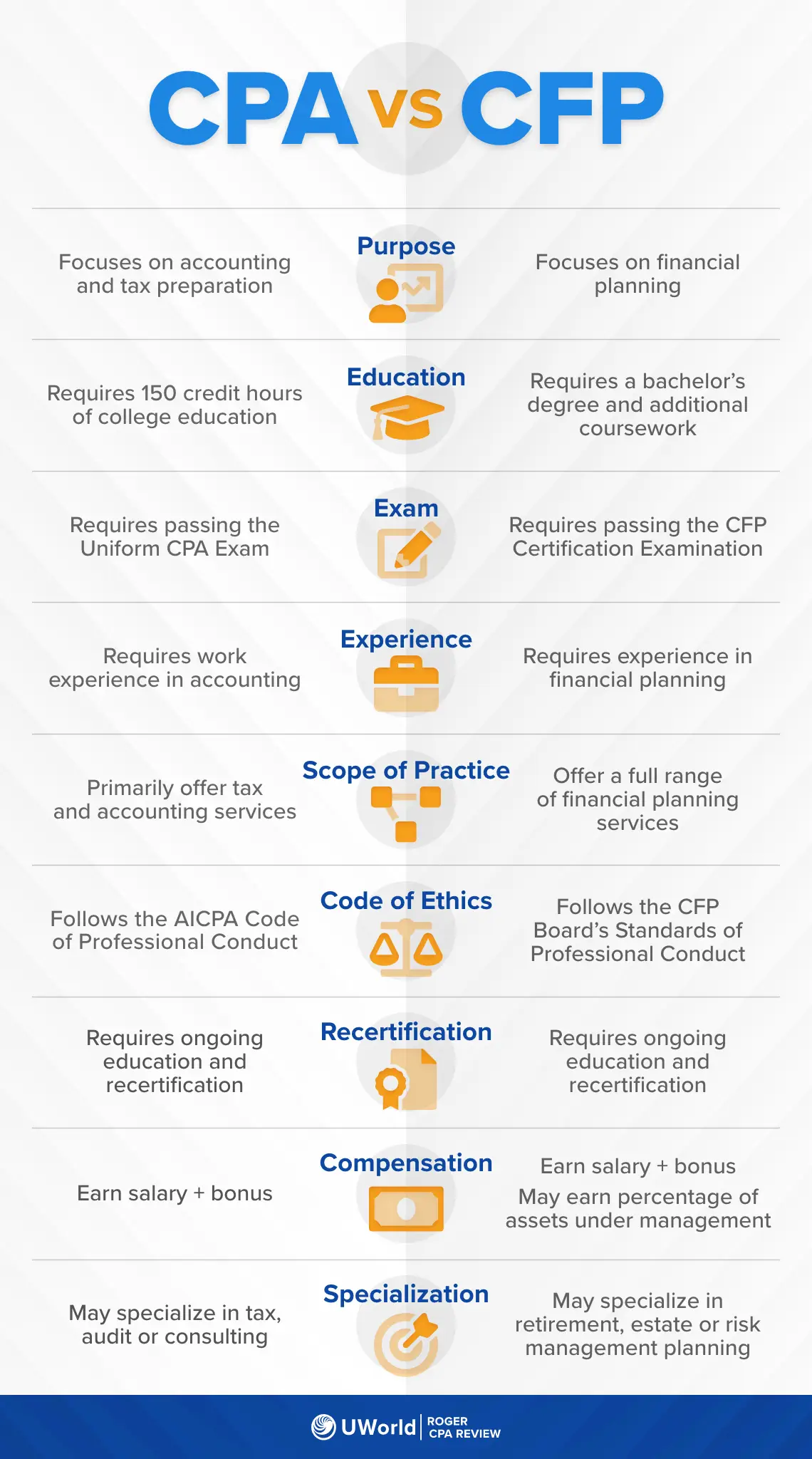

Source : accounting.uworld.com

Look, nobody’s going to hand you clients just because you passed the CFP exam. That’s a harsh reality. It’s a demanding process, designed to test your knowledge and your ethics. But does that rigor translate directly into a flood of new business? Not automatically.

What Does “CFP” Actually Mean to Clients?

To a lot of people out there, CFP might sound impressive. It probably conjures images of someone who’s incredibly smart and trustworthy. They hear “Certified Financial Planner” and think, “This is the expert I need.” They associate it with a higher standard, a Standard of quality in a sea of financial advice. This perception alone can be a powerful marketing tool for advisors who hold the designation.

Is it Just a Fancy Title?

Some argue that a CFP is just a fancy title, a way to differentiate yourself. And yeah, to a degree, they’re not entirely wrong. Plenty of highly competent advisors aren’t CFPs. But ignoring the value it brings is missing the bigger picture. It’s not just a title; it’s a symbol of a commitment to a rigorous process and ethical standards.

The “Fiduciary Duty” Angle

This is a big one. Certified Financial Planners are held to a fiduciary standard. What does that mean in plain English? It means they are legally and ethically obligated to act in their client’s best interest, always. No exceptions. This isn’t true for all financial advisors, and clients are getting savvier about this distinction. Knowing your advisor must put your needs first is a massive peace of mind booster. It separates the truly client-focused professionals from those who might be pushing products.

The Practical Difference for Your Business

So, you’ve got the certification. Now what? It can genuinely attract higher-quality clients. People seeking Full financial planning are often looking for that CFP credential. They’re willing to pay for that assurance. It can also open doors to certain firms or specific roles that require or strongly prefer advisors to have it. Think about it like a doctor specializing; it signals a deep commitment.

Source : youtube.com

Decoding the CFP Requirements: The Four E’s

Let’s get down to brass tacks. What does it actually take to become a CFP? It’s not just a weekend seminar. The CFP Board outlines the requirements, often summarized as the “Four E’s”: Education, Examination, Experience, and Ethics. Skipping any of these steps? Forget about it. This isn’t a game where you can find shortcuts.

Education: More Than Just a Degree

You need a solid foundation. This usually means having a bachelor’s degree. But the education piece goes way beyond that. You have to complete a curriculum approved by the CFP Board. This isn’t your standard college coursework; it’s dense, focused financial planning education covering everything from retirement planning and estate planning to ethics and insurance. Think of it as a specialized master’s program squeezed into a more manageable format. It’s designed to make sure you know your stuff inside and out.

The Infamous CFP Exam

This is where many advisors truly feel the heat. The CFP exam is notoriously difficult. It’s a six-hour, Full test that covers a vast array of financial planning topics. We’re talking about 170 questions, multiple-choice and scenario-based, designed to make you think on your feet. Many people fail it on their first try. Passing this exam is a significant hurdle, and it’s a badge of honor in itself. It proves you can apply complex knowledge under pressure.

Experience: Real-World Application Matters

Knowledge is one thing; practical application is another. The CFP Board requires a certain amount of relevant work experience. This isn’t just about clocking in hours. You need to have experience in financial planning and related areas. The specifics can vary depending on whether your experience is direct or indirect, but the point is clear: they want you to have actually done this work before they certify you. It ensures you’re not just a bookworm but someone who can navigate the messy reality of client finances. This practical experience is Crucial.

Ethics: The Foundation of Trust

This is non-negotiable. All CFP® professionals must adhere to the CFP Board’s Code of Ethics and Standards of Conduct. This means acting with integrity, objectivity, competence, fairness, confidentiality, professionalism, and diligence. It’s about putting the client first, always. Any ethical lapses can result in disciplinary action, including suspension or revocation of the certification. It’s the bedrock of the entire designation, ensuring that the public can trust CFP® professionals.

The Costs: Beyond Just Tuition Fees

Let’s talk money. Getting your CFP isn’t cheap. There are fees for the education courses, the exam itself, and ongoing renewal fees. It adds up, and you need to budget for it. But the cost isn’t just financial; it’s also about your time. Think of all the hours you’ll spend studying when you could be working or with your family.

Financial Investment Breakdown

First, there’s the education requirement. Approved education programs can cost anywhere from a couple of thousand dollars to upwards of $10,000, depending on the provider and format. Then comes the exam application fee, which is several hundred dollars. If you don’t pass the first time (and many don’t), you’ll have to pay to retake it. Add to that the initial certification fee and then the annual renewal fees. It’s a significant financial commitment over time. Don’t forget potential study materials or review courses, either!

The Time Commitment is HUGE

This is often the bigger hurdle than the money. Studying for the CFP exam requires hundreds of hours. We’re talking about late nights, skipped weekends, and a serious dedication to absorbing a massive amount of information. Even after you get certified, staying current with continuing education requirements takes ongoing time. If you’re already juggling a full client load, carving out this study time can feel almost impossible. It’s a marathon, not a sprint, requiring serious personal sacrifice.

Opportunity Cost: What Are You Giving Up?

Every hour you spend studying is an hour you’re not spending with clients, prospecting for new business, or perhaps enjoying downtime. This opportunity cost is real. For some advisors, especially those just starting out, the immediate financial strain and the diversion of focus from income-generating activities can be daunting. You have to weigh the potential future benefits against the immediate sacrifices you’re making right now. Is the payoff worth the present hardship?

Does the CFP Really Boost Your Career?

Okay, so it’s tough and it costs money. But does it actually move the needle on your career? For many, the answer is a resounding yes. It’s a signal to the market that you’re serious, qualified, and committed to a high standard of practice. It can open doors that might otherwise remain shut.

Attracting Better Clients, Period.

This is often cited as the biggest win. When you market yourself as a CFP® professional, you’re speaking a language that many sophisticated clients understand. They see the designation and immediately associate it with expertise, trustworthiness, and a commitment to their best interests (that whole fiduciary thing again!). This can lead to attracting clients who are more serious about planning, have higher net worth, and are generally easier to work with. You’re less likely to deal with tire-kickers.

Enhanced Credibility and Trust

Let’s face it, the financial services industry has had its share of bad actors. The CFP mark helps cut through that noise. It’s a globally recognized mark of excellence. When prospective clients see it, their trust in you automatically increases. It’s like a pre-vetting process. They know you’ve met rigorous standards. This enhanced credibility can significantly shorten the sales cycle and build stronger, longer-lasting client relationships. People want to work with professionals they can trust implicitly.

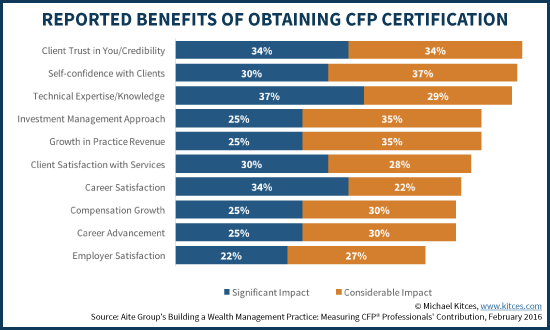

Source : kitces.com

Career Advancement Opportunities

Some firms actively seek out advisors with the CFP certification. It might be a requirement for certain senior roles or leadership positions. It can also make you a more attractive candidate for independent broker-dealers or Registered Investment Advisors (RIAs) looking to build a team of highly qualified professionals. The designation signals a level of professionalism and dedication that many employers value highly. It’s a tangible asset on your resume and LinkedIn profile.

Networking with Peers

Being part of the CFP community means you’re connected with thousands of other professionals who are serious about financial planning. The CFP Board often facilitates networking opportunities, conferences, and professional development events. This network can be incredibly valuable for sharing best practices, seeking advice, and even finding referral partners. You’re joining an elite group of professionals dedicated to advancing the field.

The Downsides and Criticisms: It’s Not All Sunshine

But let’s not pretend the CFP is a magic bullet. There are valid criticisms and downsides to consider. Not every advisor needs it, and sometimes the focus on the designation can overshadow other Key aspects of being a great advisor.

The “Not Required” Argument

This is a big one for many. The CFP Board requires a degree, specific coursework, an exam, and experience. But here’s the kicker: you don’t legally need to be a CFP to give financial advice. Many successful advisors operate without the designation, focusing on other licenses or specializations. The requirements can feel like a barrier erected by the CFP Board itself, not necessarily a universal requirement for quality financial advice.

Cost vs. Benefit: Is It Always Worth It?

For some advisors, especially those in niche markets or commission-based roles, the Large cost and time investment might not yield a proportional return. If your business model doesn’t rely heavily on Full financial planning fees, or if your target clients don’t particularly value the CFP mark, then the return on investment might be questionable. You need to honestly assess if the ROI makes sense for your specific practice.

Focus on Theory Over Practice?

Some critics argue that the CFP curriculum and exam, while Full, can sometimes lean heavily on theoretical knowledge. Does memorizing complex tax code provisions or estate planning strategies automatically translate into successfully helping a real-life family navigate a market downturn? Perhaps not always. The practical application of knowledge, empathy, and communication skills are just as Key, and these aren’t always directly measured by the CFP process. It’s easy to get bogged down in the academic side.

Potential for “Over-Certification”

In a world where clients are increasingly confused by financial jargon and credentials, is there a risk of having too many letters after your name? Sometimes, a simpler message is more effective. Constantly chasing new certifications can also distract from the core business of building relationships and serving clients. The focus should always remain on the client’s needs, not just on accumulating credentials. It’s about substance, not just symbols.

CFP vs. Other Designations and Licenses

The CFP isn’t the only game in town. There are numerous other designations and licenses available to financial advisors. Understanding how the CFP stacks up against them is Key for making an informed decision about your professional development path.

The RIA and Series Licenses

Many advisors operate under an RIA (Registered Investment Advisor) model and hold licenses like the Series 7 and Series 66. These are foundational licenses required by regulators. While Needed for practice, they don’t carry the same weight of Full planning and ethical commitment as the CFP mark. They’re about regulatory compliance and the ability to offer specific investment products, not necessarily about Overall financial planning expertise.

Specialized Designations (ChFC, CFA, etc.)

There are other respected designations out there. The Chartered Financial Consultant (ChFC) is quite similar to the CFP, offering a broad financial planning education. The Chartered Financial Analyst (CFA) designation is highly respected, particularly for those focused on investment management and analysis. Each has its own focus, rigor, and target audience. The CFA, for example, is much more investment-centric than the CFP, which is broader financial planning. Deciding which path to take often depends on your career focus.

What About Just Being “An Advisor”?

Many advisors simply operate with their basic licenses and perhaps a few specialized product training certifications. For them, the value proposition of a CFP might not Match with their business model or client base. If you’re primarily focused on selling specific insurance products or mutual funds, the CFP’s emphasis on Full, fee-based planning might be overkill. It’s about finding the right credential for the right business model and target market. You don’t need a hammer to turn a screw, after all.

A Look at the Numbers: Does CFP Pay More?

Source : thewallstreetschool.com

Let’s get down to the nitty-gritty: compensation. Does holding that coveted CFP mark actually translate into a bigger paycheck? The data suggests that, on average, CFP® professionals tend to earn more than their non-certified counterparts. But remember, correlation isn’t causation. Many factors influence income.

Average Salary Data

Studies and surveys from organizations like the CFP Board and industry publications often show a salary premium for CFP professionals. This premium can vary widely based on experience, location, firm type, and client base. However, the trend is generally upward. Advisors with the CFP designation often report higher average incomes, potentially ranging from 10% to 50% more than those without it, depending on the specific study and role. This income boost is a significant draw.

Why the Pay Bump?

Several factors contribute to this potential pay increase. As mentioned earlier, CFP professionals often attract higher-net-worth clients who tend to generate more fees. Their commitment to a fiduciary standard can also lead to deeper client trust and longer relationships, resulting in more assets under management over time. Furthermore, the advanced knowledge and Full planning skills acquired during the CFP process equip advisors to handle more complex financial situations, justifying higher compensation. Firms also recognize the value and marketing power of the designation.

Considering the Costs and Time

It’s Key to weigh this potential pay increase against the costs we’ve already discussed – the financial investment and the significant time commitment. Is the projected increase in earnings sufficient to justify the upfront expenses and the opportunity cost of the study time? For many, the answer is yes. But for others, the math might not add up, especially in the short term. You need to run your own numbers.

| Factor | CFP® Professional | Non-CFP® Advisor |

|---|---|---|

| Client Perception | High Trust, Sees as Expert | Varies Widely; May Lack Clear Signal |

| Fiduciary Standard | Mandatory | Varies; May Operate Under Suitability Standard |

| Education Requirements | Rigorous Board-Approved Curriculum | Varies; Basic Licensing or Other Certifications |

| Exam Difficulty | Extremely High (6-Hour Full Exam) | Varies; Licensing Exams are Standard |

| Work Experience | Mandatory, Specific Requirements | Varies; Licensing Requirements Apply |

| Average Income Potential | Generally Higher | Varies; Can Be Lower or Comparable |

| Continuing Education | Mandatory (30 hours/year), Ethics Focus | Mandatory for Licenses, Varies by Designation |

Who Should Absolutely Get Their CFP®?

So, who’s the ideal candidate for this whole CFP Effort? If you’re nodding along to these points, you might be a perfect fit. It’s for the advisor who wants to build a long-term, sustainable practice focused on deep client relationships and Full advice.

The Full Planner Wannabe

If your passion is truly helping people map out their entire financial lives – from saving for retirement and college to planning for taxes and leaving a legacy – then the CFP is likely your path. It’s built for advisors who see financial planning as more than just picking stocks. This designation provides the framework and the credibility needed for that Overall approach.

The Independence-Seeking Advisor

Many advisors seeking true independence and control over their practice find the CFP designation Key. Operating as a Registered Investment Advisor (RIA) often goes hand-in-hand with the fiduciary standard, which the CFP embodies. Holding the CFP mark can enhance the reputation and trustworthiness of an independent firm. It signals to clients that you’re committed to their best interests, not just selling products.

The Career Climber

If you have aspirations of moving into leadership roles, managing a team, or working for a firm that emphasizes high standards of financial advice, the CFP certification can be a significant advantage. It demonstrates a commitment to professionalism and expertise that many senior management positions look for. It’s a clear signal of your dedication to the profession.

The Ethical Purist

For advisors who are deeply committed to the fiduciary standard and believe strongly in putting clients first above all else, the CFP is a natural fit. It aligns your professional identity with your core values. You want clients to know, without a doubt, that you are operating in their best interest. The CFP mark is a powerful, tangible way to communicate that commitment. It’s about building a business on a foundation of unwavering integrity.

Who Might Want to Skip the CFP?

Conversely, not everyone needs to chase this certification. There are valid reasons why an advisor might decide the CFP isn’t the right move for them. It’s about understanding your own career goals and business model.

The Product-Focused Salesperson

If your primary role involves selling specific financial products, like insurance or certain types of investments, and you operate under a suitability standard rather than a fiduciary one, the CFP might not Match with your business. The extensive financial planning curriculum could be less relevant than specialized product knowledge. Focus your efforts elsewhere if this describes your current role.

The Investment Specialist (CFA Track)

For individuals who are laser-focused on investment analysis, portfolio management, and quantitative research, the CFA designation might be a more appropriate and valuable pursuit. While CFPs cover investments, the CFA is far more in-depth in this specific area. If your passion is deep investment strategy, consider the CFA path.

:max_bytes(150000):strip_icc()/Cfp_final-cdafe29d5d7046c9913d6ceb1ac9c380.png)

Source : investopedia.com

The Advisor with Limited Time/Resources

Let’s be blunt: the CFP requires a significant investment of time and money. If you’re already stretched thin, perhaps just starting your career, or have Large personal financial constraints, undertaking the CFP process might be unrealistic. It’s okay to prioritize building your client base and stabilizing your business first. You can always pursue the CFP later when you have more bandwidth.

The Advisor in a Niche Market

Some advisors serve very specific niche markets where clients may not highly value or even recognize the CFP designation. For example, an advisor solely focused on servicing young professionals with basic budgeting and savings advice might not see the ROI from a CFP. Understanding your specific clientele and what they value is key. Don’t pursue it just for the sake of it if your clients don’t care.

Making Your Final Decision: It’s Personal

The decision of whether or not to pursue CFP certification is deeply personal. It depends on your individual career aspirations, your business model, your target clientele, and your willingness to commit the necessary resources. There’s no single right answer for every financial advisor.

Weighing the Pros and Cons Realistically

Take a hard look at the benefits: enhanced credibility, potential for higher income, better client acquisition, and a commitment to ethical standards. Then, consider the drawbacks: the significant financial cost, the intense time commitment, and the fact that it’s not a legal requirement. Compare these points against your own situation. Are the potential gains worth the undeniable sacrifices? This requires honest self-assessment.

Consider Your Firm’s Stance

What does your current or prospective employer think about the CFP? Some firms actively encourage and even subsidize the process for their advisors. Others might be indifferent. Understanding your firm’s perspective can influence your decision, especially if they offer support or if the certification is seen as a requirement for advancement within their structure. Talk to your manager!

Look at Your Ideal Client

Who do you want to work with? If you envision serving high-net-worth individuals or families seeking Full financial planning, the CFP mark will likely serve you well. It’s a signal that resonates with that demographic. If your ideal client is different, perhaps focused on basic banking services or specific investment products, the CFP’s value proposition might be less pronounced. Remember, the White Coat Investor often advises considering your specific audience and goals. It’s about alignment.

Your Long-Term Vision

Where do you see yourself in 5, 10, or 20 years? Do you want to be a thought leader in financial planning? Run your own independent RIA? Move into a corporate advisory role? The CFP certification can be a powerful tool for achieving many different long-term career goals within the financial advice industry. Think about the kind of advisor you aspire to be and whether the CFP fits that vision. It’s a stepping stone, but is it the right one for your future?

Frequently Asked Questions

Is getting a CFP certification worth it for financial advisors?

Totally! For most advisors, pursuing a CFP certification is a Shift. It significantly boosts your credibility, opens doors to higher-paying clients, and deepens your knowledge. Plus, it shows a serious commitment to ethical practices. It’s a big undertaking, but the career rewards are usually well worth the effort.

What percent of advisors have their CFP?

Because it’s such a rigorous process, only a fraction of financial advisors actually hold the CFP designation. While exact numbers fluctuate, it’s generally estimated that somewhere between 20-25% of all financial advisors in the U.S. are CERTIFIED FINANCIAL PLANNERS™. It’s a mark of distinction, for sure.

Is $200,000 enough to work with a financial advisor?

Yeah, $200,000 is often enough to get started with a financial advisor, especially those who specialize in working with clients building their wealth. Some advisors might have higher minimums, but many welcome clients with that amount. You might find advisors who charge a flat fee or a percentage, so it’s good to shop around. But don’t let the number scare you; many advisors are happy to help you grow your assets.

How long does it take to get a CFP certification?

It’s not a quick process, man. Generally, it takes several years. You’ll need a bachelor’s degree, plus a significant amount of relevant work experience – usually a few years. Then there’s the coursework and finally, passing that beast of an exam. So, all in, we’re talking a minimum of 5-7 years from starting your career to getting that CFP mark.

What’s the difference between a financial advisor and a CFP?

Think of it this way: all CFPs are financial advisors, but not all financial advisors are CFPs. A CFP has met specific education, exam, experience, and ethical requirements set by the CFP Board. It’s a professional designation that signifies a higher level of expertise and a commitment to fiduciary duty. A general financial advisor might not have gone through that rigorous process, so the CFP mark means a lot.

Can a CFP advisor charge commissions?

This one’s a bit tricky. Traditionally, CFPs are held to a fiduciary standard, meaning they must act in their client’s best interest. However, the rules have evolved, and some CFPs can operate under different compensation models, including commissions, depending on their registration and the specific services they offer. But, many clients prefer fee-only CFP advisors because it removes potential conflicts of interest. Always ask your advisor upfront how they are compensated.

0 Response to "Is Getting A Cfp Certification Worth It For Financial Advisors"

Post a Comment